Feature: BQE Water

BQE Water provides innovative water treatment solutions to the mining industry, helping its customers build environmentally sustainable water management systems. The company is headquartered in Vancouver, with regional offices in Chile and China. It has been in operation for over 25 years, serving many of the leading global mining companies. The company has designed and built 30 water treatment plants globally and has developed and commercialized four proprietary technologies.

It should be said that BQE Water is a very small company having a market cap of approximately $70M – making it a microcap company and at the small end of the companies that we invest in. The company has no bank research coverage and no institutional investors in its investor base. Its shares are also closely held, with ~54% of the shares held by management, the board of directors, and other insiders.

History

The company began in 1997, originally incorporated as Biomet, with the purpose of developing the BioSulphide process for the treatment of industrial waste. As part of going public in 2000, the company changed its name to BioteQ Environmental Technologies. Dr. David Kratochvil was part of the founding management team as Manager of Engineering and Development. Today, he is the President and CEO.

The early business model had the company build, own, and operate water treatment plants and receive revenue from selling the metals recovered as part of the treatment process. Building and owning water treatment plants was a capital-intensive business. The revenue was also unpredictable, tied to metal recovery rates and commodity prices.

After a rough period of project challenges and legal disputes between 2010 and 2013, the board went through a refresh, with Peter Gleeson becoming Executive Chair and Dr. David Kratochvil rejoining (after a very brief departure) as President and CEO. A restructuring was done to realign the cost structure, and a new business model was implemented. The new model would be less capital intensive and would focus on recurring revenue services, highlighting the BioteQ team as technical experts and technology partners for their customers.

In March of 2017, the company changed its name to BQE Water, and in 2018 the business was finally turned around, with no debt and improved profitability.

BQE Water Today

The company monetizes its intellectual property through services that span the full life cycle of mining projects, from pre-permitting to post-closure. The company’s primary service is the long-term operation of water treatment plants, designed by their team, to generate recurring revenues linked to plant performance. They also generate revenue from technical services that are project-specific and non-recurring in nature.

The business has two main segments: Operational Services and Technical Services.

Operational Services

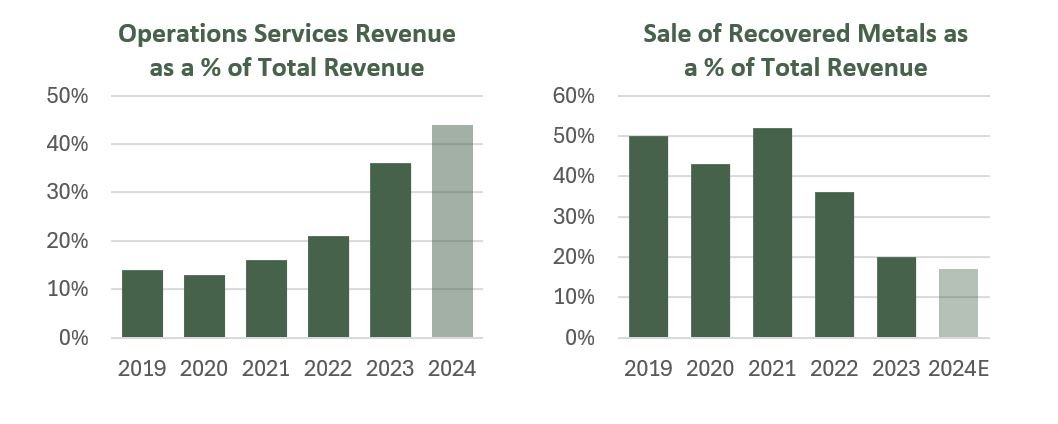

Revenues from operational services are recurring in nature and earned through water treatment fees or support fees. We expect recurring revenue from operational services to grow meaningfully as new projects come online. While contracts for these services can vary between 1-5 years, they almost always renew while the mine is in operation, making them valuable long-term streams of revenue. Margins in this business are also very attractive, usually >50% gross margins once the plant is fully commissioned.

The company also monetizes its intellectual property through joint ventures (in China) by sharing the value of metals recovered from treating water. While this continues to be part of the business today, it is not an area of focus for the company, and we expect it will be a much smaller part of the business in the future.

Technical Services

The technical services revenue is based on consulting services that address specific water management issues. These services can include feasibility and assessment studies to help clients meet regulatory conditions during the permitting phase.

As technical experts, the company is in a very good position to win the operational work when the project is ready for development. The gross margins in this business are also quite strong at 45-55% depending on the type of work performed. While this part of the business is less scalable, we see it as an efficient way for the company to demonstrate its expertise and pre-qualify projects that have strong potential to build operational recurring revenue in the future.

Management Team and Board

We have a positive view of the management team – having met with David Kratochvil, President and CEO; Heman Wong, CFO ; Daniel Cook, Director of Operations; and Peter Gleeson, Executive Chairman.

Many of the senior team members have been with the company for over a decade and were key in the successful turnaround and repositioning of the business.

The team’s struggle during the 2011-2013 period has instilled a few lessons that help govern their business today. The organization remains cost conscious and has kept overhead expenses in check. They have also become much more selective about the projects they work on, both as a function of prioritizing the best opportunities and also thinking about these clients as potential long-term partners. The balance sheet is also conservatively managed, something that we expect to continue as management values the security of having no debt and maintaining cash on hand.

The board and senior management own 26.6% of the shares outstanding, creating a strong alignment with shareholders. Other insiders (two individuals), who are aligned with the board, own another 27% of the shares.

Industry Dynamics

The mining industry has always used water as part of mineral processing and today about 90% of mining processes require the use of water to extract resources. The industry has several challenges including:

Climate Change – There is often not enough water at mining sites to use for processing, making it important to find ways to recycle water. The climate is becoming more erratic, making wet and dry periods more extreme, creating additional challenges.

Government Regulation – Rules are getting stricter following a series of accidents in the industry. Limits to water storage will mean that more water needs to be treated and discharged. Tighter limits are being imposed on the level of contaminants that can be safely discharged, requiring more complex solutions to obtain environmental permits. Regulations are also requiring increased financial bonding for projects to deal with accidents, mine closures and environmental restoration.

Social Licence – Mining companies require a social licence to operate within communities and they need to be seen as stewards of water resources and not polluters. This requires companies to have a serious water management plan that eliminates risks to the community and the environment.

The world needs more critical minerals, and mining companies need help in dealing with increasingly complex water management issues. BQE Water has seen an increase in demand for its services, and we expect that this demand will remain strong for years to come.

The Investment Case

Growing Recurring Revenue

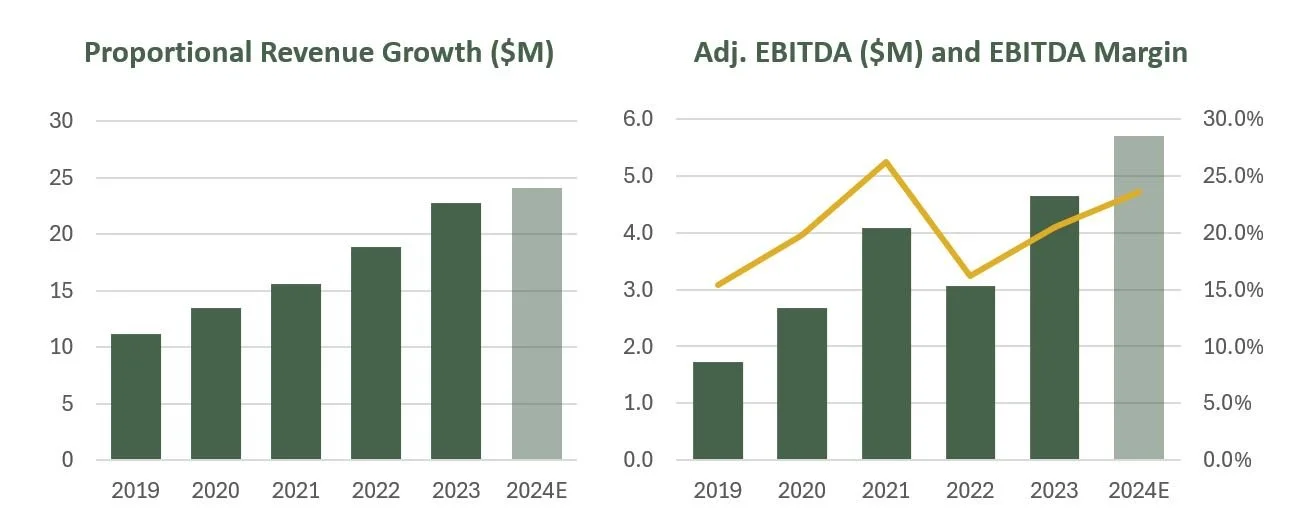

We really like long-term recurring revenue streams. They are more predictable and can be undervalued by investors who are only looking at the short-term. BQE can efficiently grow without the need for capital (the mining companies cover the capex and own the plant), so the limiting factor will be the pace at which BQE and their mining clients can bring new plants online. The company has signalled that it can commission, on average, two plants a year and that it could, in time, increase this number as it brings on or develops more experienced project managers.

Revenue per plant can vary widely, from as little as $0.5 million to $2.0 million in revenue per year depending on the size, the volume of water treated, and the running time of the plant (seasonal vs. year-round 24/7). We are expecting approximately $2 million of additional operations revenue per year based on BQE’s current pipeline of opportunities.

From 2018 to 2023, the operations revenue grew at a 42% compound annual growth rate (CAGR). While we anticipate strong growth to continue, we expect this segment to grow in the 20% range given the larger base of business it has today.

Essential Service

We like that BQE Water performs a critical service to the mining process, but at a cost that is not large compared to the entire project. We believe that operating in an environment where there is a high cost of failure and where technical expertise is required, will allow for sustainable high margins.

The Competitive Moat

Intellectual Property and Know-How

BQE Water has patents and proprietary know-how, giving it a competitive advantage over their peers. For example, they have developed the only non-biological treatment for selenium – making this treatment more accessible, as biological treatments are hard to turn on and off and generate additional waste associated with the process.

BQE Water also has experience using their technology at scale for decades, making it harder for any new entrants to compete with them. Larger players are focused on the bigger municipal water opportunities and are less interested in partnering with mining companies to do the technical work upfront. BQE does compete with larger players – but 60% of their work is sole-sourced and relationship-based, meaning that most of the time they are not competing with anyone directly.

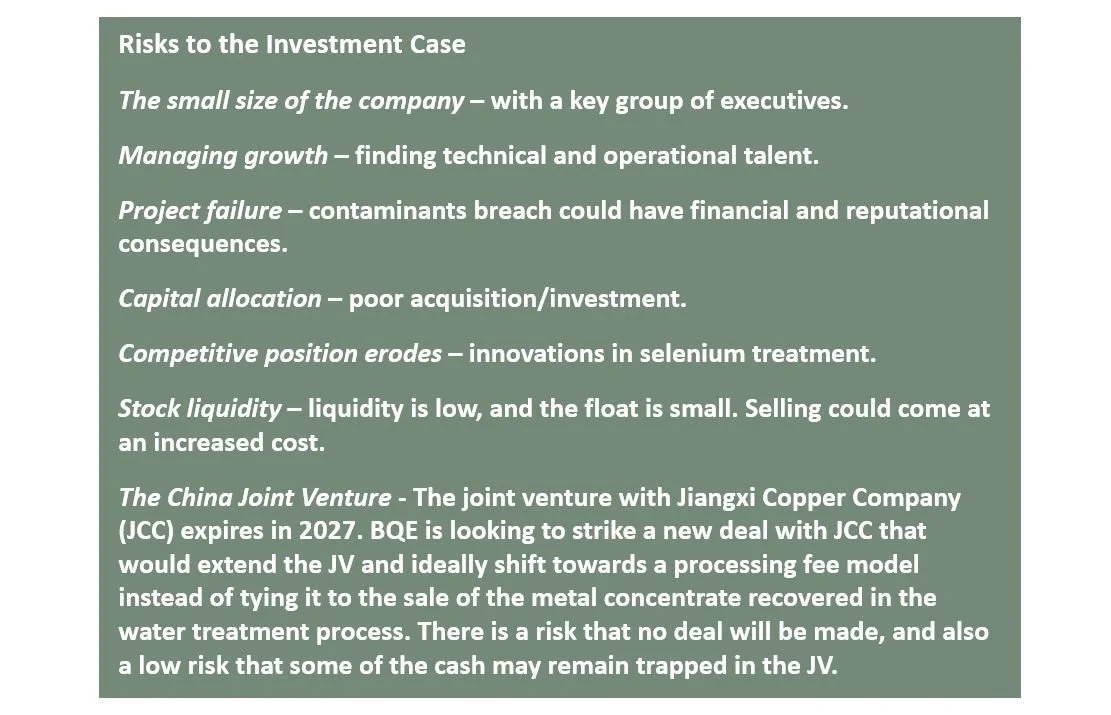

At the same time, we acknowledge that Veolia and Evoqua are much larger than BQE and have competing solutions in every category (except non-biological selenium). We consider BQE Water’s competitive advantage here to be modest but stable, given the competitive intensity is low.

Switching Costs

The company’s operational services contracts are somewhat short (1-5 years) but there are real switching costs associated with attempting to replace the services. BQE’s technical know-how comes with assurances on volume and quality standards. There is also very little incentive to switch once a plant is in operation. The only real alternative is to take the process in-house, which involves staffing and training costs along with a greater risk of failure. BQE Water has been operating at the Raglan Mine in Northern Quebec for over 20 years, even as the mine changed ownership several times.

Optionality

Company Maker Projects

BQE Water mentions in its presentation material the potential for several “company maker” projects. These are larger operations that they have performed some technical work on over the years. The company provides an example of the potential size, indicating that one of the large projects could be $3.5M+ in operations revenue per year on a mine site that has a 30+ year operating life.

While the company does not explicitly disclose these projects, there are breadcrumbs to follow from publicly available information. A notable example is Seabridge Gold’s KSM project in B.C., the largest undeveloped gold and copper mine in the world, where over $1 billion has been spent to advance the project. Of this amount, $444 million has been spent since 2021 to achieve the project's “substantially started” designation, which was received in July of this year, securing its Environmental Assessment Certificate from the B.C. government for the life of the project.

The project has a large water treatment component, and BQE Water has been working with Seabridge for years. Given its scale, the KSM project requires more than $6B in capital to put it into production, making financing a considerable challenge. However, with the price of gold near all-time highs, the project's after-tax internal rate of return (IRR) has improved significantly.

We do not assign a high probability to the KSM project being built, the project needs partners or buyers with very deep pockets. There are several other similar “company maker” projects that BQE could also win. Though timelines and probability of success are hard to assess for these opportunities, BQE continues to perform technical work on projects of all sizes. We like the free option that these mega-projects add to our investment case for the company.

Increased Selenium Regulation

BQE Water's leadership in selenium treatment technology is well-recognized throughout the mining industry. The company is positioned to benefit from stricter selenium regulations, particularly in North America. Furthermore, potential new regulations in Central and South America could provide additional upside to our investment case for BQE Water.

Capital Allocation

The company has approximately $8M in cash on their nearly debt-free balance sheet. While the company has previously executed share buybacks in 2023 and could consider initiating a dividend, we expect management to prioritize growth initiatives, including potential acquisitions.

Based on discussions with management, a small acquisition where they could acquire a business with a strong skillset to complement their existing capabilities would be ideal. Although we have not factored an accretive or strategic acquisition into our base case, the company’s excess capital provides multiple avenues for creating long-term shareholder value.

Take-Out Target

The water industry is a very attractive area for strategic buyers and private equity firms. In 2023, H20 Innovations, another Canadian-listed water company, was taken out by a private equity firm at 20x EV/EBITDA.

If BQE Water continues to grow like it has been, with its very strong margins and capital light model – it will garner the attention of many interested buyers. However, we view potential acquisition interest as both an opportunity and a risk, preferring to see the company continue its independent growth trajectory.

Valuation

We look at the valuation for BQE Water in a few different ways. Our base-case discounted cash flow (DCF) approach using modest growth (mid-teens overall revenue growth) and conservative margins arrives at what we believe is a conservative $80 share price. In this scenario, the company continues to build recurring revenue by adding a series of smaller plant operations, while continuing to grow its technical services business.

We generally like to see more upside than this with our base case scenario, but we view the likelihood of one or more of the larger projects coming online over the next five years as increasingly probable. This is because the company continues to work on many projects, and any of these could materialize into larger undertakings through time. In some of these upside scenarios, the share price could easily double from today’s value.

On a shorter-term EV/EBITDA multiples basis, the company is trading at about 8x and 7x our base-case estimates for 2025E and 2026E, respectively. We think that is attractive given the recurring nature of the revenue (>45% recurring revenues in 2026E) and strong EBITDA margins (~27% in 2026E). We think the right multiple range for a growing water technology business with recurring revenue and good margins is in the 10-14x forward EV/EBITDA depending on the strength of the growth trajectory.

We believe the fundamental downside would be moderate given the recurring nature of the operations business and that some of the technical services revenue is generated under planned master service agreements (MSAs).

Summary

BQE Water is an example of our process that seeks to find quality companies very early. Despite its microcap status and limited investor visibility, it checks a lot of boxes for us. It can be hard to find a company with a strong management team, operating a very good business model in an industry that has multiple tailwinds.

The downside of being early and taking a long-term view, is that it often requires patience. We have realistic expectations for growth and how long it can take for mining projects to come online, so we know this could take time to develop.

Looking forward, BQE Water's capital-light business model supports our projection of 20%+ return on invested capital (ROIC). At this pace, this compounding should be very good for shareholders who have patience and are thinking long-term.